Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Recent Data Draws Bleak Prospect for Iraq Next Year

The Iraqi economy has been in a bad shape and, in the short term, it is going to get worse; nothing new about this and there is almost a consensus about it despite differences in the cited material’ verifiable evidence, manifestations and root-causes for such a degenerating situation.

A “multi-whammy” combination, or association, of effective impacting factors and circumstances played their part in what the country has been and is facing. These include political instability and divisions; fragile security conditions; vulnerability of high-dependency economic structure; bad and inefficient management and decision making; kleptocracy governance coupled with hyper corruption, particularly the formalized and institutionalized; and impacting external intrusion, among others.

Data and information on these factors and circumstances are massive, and hardly any day passes without adding new items to the long list of cases and examples reported by the media, formal entities, experts and legal authorities; the apparent outcome of all that is a severely deteriorated economy of Iraq.

Data I compiled from a recent IMF report regarding main macroeconomic indicators are presented in the table, which you can view in this pdf. The table provides the progression of 26 macroeconomic indicators over the last two decades using three different sets of data: the first is the average, of a long and rather up-normal period 2000-2016; the second, annual data for each of the last three years 2017:2019, and the third are projections for 2020 and 2021.

The focus in this brief contribution is on the prospects for the economy in this and next year, in comparison with the last three years.

Mr Jiyad is an independent development consultant, scholar and Associate with the former Centre for Global Energy Studies (CGES), London. He was formerly a senior economist with the Iraq National Oil Company and Iraq’s Ministry of Oil, Chief Expert for the Council of Ministers, Director at the Ministry of Trade, and International Specialist with UN organizations in Uganda, Sudan and Jordan. He is now based in Norway (Email: mou-jiya(at)online.no, Skype ID: Ahmed Mousa Jiyad). Read more of Mr Jiyad’s biography here.

By Ahmed Tabaqchali, CIO of Asia Frontier Capital (AFC) Iraq Fund. This article was originally published by the LSE Middle East Centre.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Between a Rock and a Hard Place: Iraq’s Political Class’ Dilemma between Budget Realties and Protestor Demands

The twin shocks of the effect of coronavirus on the world economy and the current oil price war will stress Iraq’s budget to the limit, and lead to an economic crisis if it continues for an extended period.

While as extraordinary shocks they were unforeseeable, the Iraqi budget’s structural imbalance would have inevitably led to such an economic crisis – the only question being when and not if.

A low oil price environment exposes the structural faultiness of the budget with projected revenues not covering current spending, which is mostly composed of salaries, pensions and welfare spending. These have increased from 50% of current expenditures in 2004 to an estimated 81% in 2019, and likely to more than 85% in 2020.[1] As such the default choice for the government would be to cancel all investment spending, especially non-oil investment spending, and resort to borrowing.

Such measures have allowed the government to continue functioning, but these come at a huge cost to the economy as Table 2 below shows. Global debt markets are not as accommodating as they were in 2014-17 given Iraq’s estranged relationship with the US and the change in the IMF’s stance toward Iraq. As such the government would have to resort to domestic sources, which ultimately means indirect monetary operations by the CBI at the expense of the its foreign reserves as happened in 2014-16.

Moreover, these measures would only postpone and not resolve the crises, needing much higher oil prices to contain or mask it like in 2017-19. Medium-term oil prices would probably (for Brent prices) settle within a range of $50-60/bbl, which should partially relieve the stress on the budget, but not the need to address its imbalance.

Iraq’s 2019 budget, initially proposed by the prior government, submitted with minor changes by the current government and approved by the current parliament, perpetuated the same deficiencies and weaknessess of all Iraq’s budgets since 2003. Crucially, it deepened the structural imbalance between the budget’s current and investment expenditures, in which public sector wages consumed an ever-increasing share of government revenues.

Moreover, it undermined and reversed most of the small, but essential, fiscal reforms agreed with the IMF in the 2016 Stand-By Agreement (SBA) to address this structural imbalance; and which needed considerable follow-up reforms over the years to put the country on a sustainable path to growth and reduce the economy’s vulnerabilities to the volatile oil market. The extent of these vulnerabilities came to the fore during the collapse in oil prices in 2014, and coupled with the cost of the ISIS conflict, this led to a sharp contraction to the non-oil economy in 2014-17.

Undeterred by these memories, the budget’s planners, buoyed by the bounty of higher oil revenues, from late 2017 embarked on an expansionary budget that magnified these very vulnerabilities. This was achieved by simultaneously reversing the growth of non-oil revenues and by increasing current spending. Non-oil revenues decreased in both absolute terms and as a percentage of total revenues: -18% and -29% respectively in 2019 and 2018.

Additionally, 25% of these non-oil revenues were in fact oil-related in the form of taxes on foreign oil companies and the budget’s share from profits from the state’s oil companies. Current spending increased by 15% with the salary and pensions component growing by 7.5% instead of decreasing continuously.

The budget’s trumpeted increase of 29% in investment spending hides the fact that only 43% of this total spending for 2019 was earmarked for non-oil investment, which would nevertheless increase by 43% in 2019. However, historically this spending is on paper only, with an execution rate of under 65%. The performance in 2019 was much worse than normal with non-oil investment spending at about IQD 3.3 trn as of November 2019 from a planned budget of IQD 14.0 trn, or about a 24% execution rate.

The budget planners’ aims for 2020 were for a continuation of the expansionary budget of 2019, which dismayed the IMF enough for it to issue a critical country report (19/248) – the first since 2004. Adding to the dismay was the fact that the government’s plan for fiscal probity was based on expectations of continued high oil prices, as well as sticking to its historic under-execution of the budget. Essential budget reforms to address the structural imbalance were delegated to an expression of interest for inclusion in medium term fiscal strategy planning.

The IMF then modelled for a 2020 budget with revenues estimated at IQD 113.1 trn based on oil price assumptions of $55.8/bbl. Expenditures were estimated at IQD 123.2 trn, made up of current expenditures at IQD 99.1 trn, while oil investment spending was estimated at IQD 15.5 trn and non-oil investment spending at IQD 8.6 trn. This would have needed debt financing of IQD 10.0 trn to balance the budget. Since it’s almost impossible to cut the bulk of current spending, the government must have been anticipating a better budgetary situation through Iraqi oil prices higher than $55.8/bbl and from under-executing much needed non-oil investment spending and reconstruction.

By October, plans for budget expenditure ballooned by 31% to IQD 162.0 trn, necessitating debt financing of IQD 48.9 trn. While there are no details apart from spending and deficit figures, the political paralysis following the failure of the prime minister-designate to form a government in early March has put a halt to these runaway expenditure plans.

As long as the political class’ existential fear from the five-month long youth-led countrywide demonstrations continues to ebb and flow, this political paralysis is likely to continue. However, the main economic consequences would be the same whether a new government forms under a new prime minister-designate, or if the current caretaker government continues to limp on. The outcome either way will be that no new budget will be passed, with the government continuing to implement the executed parts of 2019’s budget throughout 2020 according to the ‘1/12th rule’.

Essentially, this means the government will continue to spend (per month) 1/12th of the actual spend in 2019 – effectively extending the current spending component for 2019 in addition to the increased spending of IQD 10.5 trn as a result of government measures to appease the demonstrators in October 2019. The government will likewise continue with the investment projects initiated in 2019.

Estimating the effects of the current events on the Iraqi budget is fraught with uncertainty. Current predictions on the extent of the decline in oil prices mirror those made following the 2014 oil price war, which then assumed a continuation of the decline into the future. This in time proved to be overly pessimistic, as will the current ‘worst-case’ prognoses. Moreover, though the effects of the new coronavirus on the world economy will be profound in Q1/2020, the extent and the continuation of these effects for the rest of the year remains uncertain.

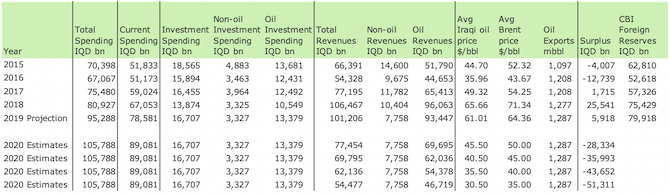

However, these negative effects would be compounded for oil prices by a sharply increased supply in an environment of weakened demand. The upshot would be an extended period of lower oil prices. The table below looks at the budget for 2015-19 and estimates for 2020 based on different realised oil prices for 2020 as whole (please see footnote 2 for notes and assumptions used).

Table 2: Iraq’s budget 2015-20. Source: Iraq Ministry of Finance[2]

Past policies of spending oil revenues on expanding the public payroll and welfare spending, in the process depleting the country’s wealth without building its infrastructure, has resulted in an economy dependent on imports of goods and services, a stunted private sector and a labour market skewed towards public employment. This development has been at the root cause of successive countrywide demonstrations. The need to urgently restructure the budget’s structural imbalances will require painful reforms and a long adjustment period, and thus would need a buy-in by the population at large.

This, given the extent of the current anti-political elite protest movement and the scale of the repression of this movement, is unlikely without significant political reform.

[1] The percentage figures are made up of salaries, pensions and transfers. Transfers are mostly composed of welfare spending and transfers to State-Owned Enterprises (SOEs) which in turn are primarily for salary payments and support to SOEs. Source: IMF Iraq country reports 2004-19.

[2] Revenues and expenditures for 2015-19 sourced from Ministry of Finance (MoF). These figures constitute revenues and expenditures actually received/made at the time and not booked. As such they differ, sometimes significantly, from those provided by the IMF. The crucial difference being that they resemble an actual cash flow statement and not an income statement. This can be seen from the difference between the Ministry of Oil’s (MoO) revenue data which show sales made and the MoF’s data which how funds received which can lag actual sales.

Iraqi oil sales and average Iraqi oil price are taken from MoO website, while average Brent prices can be found here. CBI foreign reserves are as of end of 2019 and are found here. 2019 budget numbers are as of November 2019 and projected to continue into end of 2019. Oil revenues are based on MoO data which are available as of the end of December 2019. The 2020 budget numbers assume a continuation of the budget spent for 2019. It is assumed that Iraq would maintain market share through aggressive pricing and thus that the discount to Brent would increase from $3.35 for 2019 to $4.50.

Disclaimer: Ahmed Tabaqchali’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

In the framework of the financing agreement signed yesterday by the Government of Iraq (GoI) and the European Union (EU) committing €14 million (US$15.8 equivalent) to support the government’s efforts to ensure increased and more reliable energy access for the Iraqi population, the EU and the World Bank Group (WBG) have signed today a €12.85 million (US$14.5 equivalent) implementation agreement to provide the needed technical assistance.

The initiative complements the ongoing and upcoming World Bank interventions in support of the GoI’s energy sector reforms, including those embedded in the budget support operations series (Development Policy Financing programs – DPFs), the Reimbursable Advisory Services (RAS) for structuring the Gas Value Chain and Gas Marketing in Iraq, and the support to subsidy reforms funded by the ESMAP’s Energy Subsidy Reform Technical Assistance Facility (ESRAF).

Supporting Iraq’s private sector enabling energy sector reforms is a priority development objective in the country both for the EU and the WBG. In a country where the energy sector accounts for more than 90% of central government revenues, addressing energy sector challenges is an essential and complementary action to any public finances related reforms, an area in which the European Union and the World Bank are also partnering in Iraq.

The country is also the world’s 3rd largest exporter of oil and its untapped natural gas reserves are the 12th largest in the world, yet it is forced to import fuel to meet its domestic energy demand, which imposes significant economic and fiscal strain on public finances. Equally important, Iraqi citizens are regularly faced with power shortages and have to resort to more expensive and pollutant sources of energy.

Efficiency in the management of public resources and delivery of services are critical to the achievement of public policy objectives, especially for a resource-rich upper-middle income country like Iraq, as well as fundamental to restore the trust and social contract between Iraqi citizen’s and the country’s institutions, especially in a post-conflict era of stabilisation and reconstruction. “As pledged in the Kuwait Conference, the European Union is committed to help Iraq’s reconstruction efforts and economic and political reforms to secure a better future for its citizens,”