Genel Energy plc has updated its oil reserves and resources across its portfolio.

Bill Higgs (pictured), Chief Executive of Genel, said:

“Genel’s producing assets are profitable even at an oil price of $30/bbl and this, coupled with our robust balance sheet, supports investment in growth and the payment of a material dividend. The reduction of reserves at Tawke largely relates to production towards the end of the life of the field, and consequently our mid-term production outlook is materially unchanged and there is no reserves impact on our business plan.

“Our production funds an approved but flexible capital programme that, in the right market conditions, enables us to drill the wells necessary to evaluate the potential to convert the 2C oil resources in our portfolio, validated for the first time by ERCE, into reserves and production, boosting our cash generation potential.“

Net oil reserves (MMbbls)

1P

2P

3P

31 December 2018

99.3

154.9

219.3

Production

(13.2)

(13.2)

(13.2)

Technical revisions

(17.2)

(17.8)

(11.2)

31 December 2019

68.8

123.8

194.9

International petroleum consultants DeGolyer and MacNaughton assess that on a gross basis, at the Tawke licence in the Kurdistan Region of Iraq containing the Tawke and Peshkabir fields, year-end 2019 1P reserves stood at 228 MMbbls, compared to 348 MMbbls at year-end 2018, after adjusting for production of 45 MMbbls and a downward technical revision of 75 MMbbls. Tawke licence 2P reserves stood at 400 MMbbls (502 MMbbls in 2018) and 3P reserves at 641 MMbbls (697 MMbbls in 2018).

Broken down by field, Tawke field gross 1P reserves stood at 176 MMbbls (294 MMbbls in 2018), 2P reserves at 284 MMbbls (376 MMbbls in 2018) and 3P reserves at 421 MMbbls (477 MMbbls in 2018). Peshkabir field gross 1P reserves stood 51 MMbbls (54 MMbbls in 2018), 2P reserves at 116 MMbbls (126 MMbbls in 2018) and 3P reserves at 220 MMbbls (unchanged from 2018).

Genel continues to take a conservative view of the Enhanced Oil Recovery project at the Tawke PSC, and will look to book reserves in relation to the project, which has the potential to increase recovery over the life of field, once enhanced performance has been demonstrated at the field.DeGolyer and MacNaughton has included23MMbbls of 2P and 45 MMbbls of 3P gross reserves, working interest portions of which are not included in the table above.

At Taq Taq, there is a minor technical downward revision of 2.1 MMbbls of gross 2P reserves associated with the unsuccessful TT-33 well, and these now total 44 MMbbls, with gross 1P reserves increasing by 3.3 MMbbls to 20.1 MMbbls, illustrating the continued strong underlying performance of the asset. McDaniel & Associates carried out the independent assessment of the Taq Taq licence.

Genel’s gross 2P reserves estimate relating to Phase 1A of the Sarta development remains 34.3 MMbbls.

CONVERTING RESOURCES TO RESERVES

Net oil resources (MMbbls)

1C

2C

3C

31 December 2018

36.8

73.7

121.3

Technical revisions

29.7

78.3

224.5

31 December 2019

66.5

152

345.8

Following completion of the acquisition in 2019, Genel estimated gross resources at Sarta to be c.500 MMbbls. This potential has now been validated through an external audit conducted by ERCE, who has estimated a mid-case total recoverable oil resource of 593 MMbbls, of which 264 MMbbls is classified as 2C resource. Production performance in 2020, and the results of the upcoming three well campaign in 2021, will set out a roadmap for the conversion of these resources into reserves.

The Bina Bawi oil development has been certified by ERCE as 17.1 MMbbls of 2C resources, 13.6 MMbbls of which are expected to be converted into 2P reserves should a commercial agreement be reached and FID be taken on the first phase of the oil project.

At Qara Dagh the QD-2 well will test the crestal portion of the prospect which, based on a rigorous re-mapping exercise, has a mean prospective resource estimated by Genel at c.400 MMbbls. Genel estimates that the downdip segment tested by the QD-1 well defines a 2C resource of 47 MMbbls.

Shares in Gulf Keystone Petroleum (GKP) were trading down 9.6 percent on Monday, compared to a broader market fall of 7.4 percent, as the company announced that expansion plans will be delayed due to coronavirus (COVID-19).

In a statement to the markets, the company said:

The Company has been closely monitoring the Coronavirus (COVID-19) situation in the Kurdistan Region of Iraq. Gulf Keystone’s priority is the welfare of its staff, contractors and the communities close to its operations. We remain committed to deliver safe operations, protection of the asset and the underlying business.

In an attempt to limit the spread of Coronavirus (COVID-19), the Kurdistan Regional Government, in line with many other jurisdictions, has put in place a series of tight controls on the movement of personnel into and around the region. With these controls, along with the increasing global restrictions on movement, it has become difficult to ensure Gulf Keystone has the appropriate drilling personnel and equipment on site in order to continue safe drilling operations.

Therefore, with the SH-13 well – the current well in the campaign – at a safe stage, the decision has been taken to suspend drilling activities until conditions improve to ensure safe operations.

Production rates from the field are at c.38,000 bopd and production currently continues unaffected by the impact of Coronavirus (COVID-19). However, as a precaution, the Company has restricted the access to its production facilities. As a result, certain construction activities related to the expansion to 55,000 bopd have also been suspended until circumstances improve.

The current situation is extraordinary and we believe that our actions protect the long-term value of the asset. The planned production increase to 55,000 bopd, scheduled for Q3 2020, and average production guidance for 43,000 – 48,000 bopd remain priorities.

However, the suspension of drilling and certain expansion operations may impact Gulf Keystone’s ability to meet these targets in the timeframes currently in place. Gulf Keystone will continue to closely monitor this fast-moving situation and will provide updates, as appropriate. As previously announced, the Company will release its Full Year results on 26 March 2020.

Notwithstanding the above, the Company remains in a strong financial position to manage through these turbulent times with a cash balance of $159 million, as at 13 March 2020.

Jón Ferrier, CEO, commented:

“As a Company we place the welfare of our people and those we work with and near as our absolute priority. We also have to be confident of having the right people on site to continue safe operations. Whilst we are not aware of any employees or contractors having been infected, we believe it is prudent to suspend drilling and certain production facility expansion operations during this time.

“We are watching the situation closely and will keep all of our stakeholders informed of developments. Meanwhile, the Shaikan Field itself is performing well.“

Oryx Petroleum has announced its financial and operational results for the year ended December 31, 2019.

The Corporation also announces agreements with AOG International Holdings Limited (“AOG”) to amend the Loan Agreement dated March 13, 2015 and to establish a new short term credit facility. All dollar amounts set forth in this news release are in United States dollars, except where otherwise indicated.

2019 Financial Highlights:

Total revenues of $150.5 million on working interest sales of 2,780,800 barrels of oil (“bbl”) and an average realised sales price of $48.72/bbl for 2019

– 54% annual increase in revenues versus 2018

– Q4 2019 revenues increased 14% versus Q3 2019

– The Corporation has received full payment in accordance with Production Sharing Contract entitlements for all oil sale deliveries into the Kurdistan Oil Export Pipeline through September 2019

Operating expenses of $28.9 million ($10.41/bbl) and an Oryx Petroleum Netback(1) of $18.90/bbl for 2019

– 17% decrease in operating expenses per barrel versus 2018

Loss of $59.2 million ($0.11 per common share) in 2019 versus Profit of $43.8 million in 2018 ($0.09 per common share)

– Loss in 2019 primarily attributable to an impairment expense related to the Hawler license area and an impairment expense and a provision related to the Corporation’s former interest in the Haute Mer B license area

– Profit in 2018 primarily attributable to an impairment reversal related to the Hawler license area

Net cash generated by operating activities was $28.1 million in 2019 versus net cash generated by operating activities of $8.1 million in 2018 comprised of Operating Funds Flow(2) of $26.9 million and an $1.2 million decrease in non-cash working capital

Net cash used in investing activities during 2019 was $35.1 million including payments related to drilling and facilities work in the Hawler license area, preparation for drilling in the AGC Central license area, and an increase in non-cash working capital

$8.9 million of cash and cash equivalents as of December 31, 2019

Oryx Petroleum Netback is a non-IFRS measure. See the table below for a definition of and other information related to the term.

Operating Funds Flow is a non-IFRS measure. See the table below for a definition of and other information related to the term.

2019 Operations Highlights:

Average gross (100%) oil production of 11,700 bbl/d (working interest 7,600 bbl/d) for the year ended December 31, 2019 versus 6,500 bbl/d (working interest 4,200 bbl/d) for the year ended December 31, 2018

– 80% increase in gross (100%) oil production in 2019 versus 2018; 12% increase in gross (100%) oil production in Q4 2019 versus Q3 2019

– Successful completion of four producing wells during 2019

– First successful completion of a well targeting the Cretaceous reservoir at the Demir Dagh field utilising a horizontal well design

Gross (working interest) proved plus probable oil reserves of 103 million barrels as at December 31, 2019

Environmental and Geohazard Assessments related to planned drilling in the AGC Central license area initiated and largely completed

2020 Operations Update:

Average gross (100%) oil production of 14,500 bbl/d (working interest 9,400 bbl/d) and 14,400 bbl/d (working interest 9,400 bbl/d) in January and February 2020, respectively

The drilling of a horizontal sidetrack of the previously drilled Banan-1 well in the portion of the Banan field east of the Great Zab river was completed in early 2020

Data obtained during drilling indicate that the Tertiary reservoir in the eastern portion of the Banan field contains oil of similar density to oil produced from the Tertiary reservoir in the portion of the Banan field west of the Great Zab river

Attempts to complete the well as a producer in the Cretaceous reservoir were unsuccessful

Further drilling targeting both the Tertiary and Cretaceous reservoirs is planned in 2020

Operations in recent weeks were successful in shutting off water production from the Banan-5 well which is producing oil from the Cretaceous reservoir in the portion of the Banan field west of the Great Zab river

The worldwide outbreak of the COVID-19 virus, including within Iraq, has not impacted operations. The Corporation is taking precautions to protect its employees and contractors but does not at this time expect that the virus outbreak will restrict operations

The planned drilling of an exploration well in 2020 in the AGC Central license area has been deferred. In 2019, the Corporation requested that the First Renewal Period of its Production Sharing Contract (due to end on October 1, 2020) be extended as a result of ongoing negotiations between Senegal and Guinea Bissau in relation to the accord governing the jointly-administered area offshore Senegal and Guinea Bissau. The Corporation is currently in discussions with the AGC regarding an amendment to its Production Sharing Contract that would implement the requested extension and expects the amendment to be finalised in the coming months.

2020 Forecasted Work Program and Capital Expenditures:

2020 capital expenditure forecast of $53 million (versus $106 million budget). Forecast activities consist of:

– $50 million dedicated to the Hawler license area: six wells including two wells targeting the Banan Cretaceous reservoir, one well targeting the Zey Gawra Tertiary reservoir, one well targeting the Demir Dagh Cretaceous reservoir, one well targeting the Banan Tertiary reservoir, and a completion of the previously suspended Ain Al Safra-2 well; a pipeline connecting the Banan field to the Hawler production facilities at the Demir Dagh field; storage tanks at the Hawler production facilities and pads, flowlines and infrastructure modifications needed to accommodate incremental drilling and production and to reduce operating costs

– $3 million dedicated to the AGC Central license area including studies, technical support and license maintenance costs

The forecast reflects the deferment of planned drilling in the AGC license area and the deferment of two wells and certain facilities expenditures in the Hawler license area that were included in the budget.

Extension of AOG Loan and New Short Term Credit Facility:

AOG has agreed to extend the maturity date of the credit facility provided to Oryx Petroleum in 2015 from July 1, 2020 to July 1, 2021 in consideration for the issuance of 33,149,000 warrants to purchase common shares of Oryx Petroleum. The Toronto Stock Exchange (“TSX”) has reviewed the applicable transaction materials. It is anticipated that the TSX will conditionally approve the extension five business days after the issuance of this news release.

AOG has further agreed to provide the Corporation with a $5 million short term credit facility to provide access to working capital in the event of any further delays in receiving payments for oil sales. The TSX has reviewed the applicable transaction materials. It is anticipated that the TSX will conditionally approve the short term credit facility five business days after the issuance of this news release.

Liquidity Outlook:

The Corporation expects cash on hand as of December 31, 2019 and cash receipts from net revenues and export sales will allow it to fund its forecasted capital expenditures and operating and administrative costs into early 2021. Additional capital is expected to be required to be able to both meet any contingent consideration obligations that become payable and to fund drilling in the AGC Central license area now planned in 2021.

“2019 was a good year for Oryx Petroleum. During the year we substantially increased production from the Hawler license area thanks to the successful completion of four new producing wells, increasing production from the Banan and Demir Dagh Cretaceous reservoirs. One of the four new wells was a sidetrack of the previously drilled Demir Dagh-3 well utilizing a horizontal well design that is integral to our development plans for the Cretaceous reservoirs in the Hawler area fields.

“In the AGC Central license area, that has best estimate unrisked gross (working interest) prospective oil resources of 2.2 billion barrels, we continue to prepare for exploration drilling. In 2019 we initiated and now have largely completed environmental impact and geohazard assessments with regards to our drilling plans. However, the timing of exploration drilling remains uncertain as we wait for Senegal and Guinea Bissau to agree on a renewal or extension of the accord governing the jointly-administered offshore area. We fully expect that an agreement will be reached but the timing is uncertain.

“Importantly, we completed our work in 2019 without incurring any Lost Time Injuries or having any significant releases or other adverse environmental incidents.

“Our 2020 capital program is focused primarily on the Hawler license area in the Kurdistan Region of Iraq where our program includes the drilling or re-entry of six wells and has been designed to allow us to increase production and to better define the remaining development potential of the four fields in the license. We have completed the sidetrack of the Banan-1 well in recent weeks and expect to spud a second well in the late Spring. In the AGC Central license area, our forecasted capital expenditures include costs related to studies and preparations for exploration drilling in 2021 assuming the AGC accord is renewed or extended in 2020.

“The combination of higher production and regular payments for oil sales in most of 2019 resulted in higher funds flow which together with cash on hand allowed us to fund our business in 2019 without seeking additional capital. We expect that cash on hand and cash receipts from net revenues will fund forecasted capital expenditures and operating and administrative costs into early 2021. AOG, our largest shareholder, has recently agreed to provide us with a short term credit facility to strengthen our liquidity position due to the recent delays in receiving cash payments for oil sales. Most of our capital expenditures are planned in the second half of 2020 and we are prepared to adjust our plans and consider other measures to strengthen our liquidity should recent market developments persist and should there be additional delays in cash receipts for oil sales.

“We look forward to implementing our plans safely in 2020 and to higher production in the Hawler license area while continuing to prepare for an exploration drilling program in the AGC Central license area.”

By Ahmed Tabaqchali, CIO of Asia Frontier Capital (AFC) Iraq Fund. This article was originally published by the LSE Middle East Centre.

Any opinions expressed are those of the author, and do not necessarily reflect the views of Iraq Business News.

Between a Rock and a Hard Place: Iraq’s Political Class’ Dilemma between Budget Realties and Protestor Demands

The twin shocks of the effect of coronavirus on the world economy and the current oil price war will stress Iraq’s budget to the limit, and lead to an economic crisis if it continues for an extended period.

While as extraordinary shocks they were unforeseeable, the Iraqi budget’s structural imbalance would have inevitably led to such an economic crisis – the only question being when and not if.

A low oil price environment exposes the structural faultiness of the budget with projected revenues not covering current spending, which is mostly composed of salaries, pensions and welfare spending. These have increased from 50% of current expenditures in 2004 to an estimated 81% in 2019, and likely to more than 85% in 2020.[1] As such the default choice for the government would be to cancel all investment spending, especially non-oil investment spending, and resort to borrowing.

Such measures have allowed the government to continue functioning, but these come at a huge cost to the economy as Table 2 below shows. Global debt markets are not as accommodating as they were in 2014-17 given Iraq’s estranged relationship with the US and the change in the IMF’s stance toward Iraq. As such the government would have to resort to domestic sources, which ultimately means indirect monetary operations by the CBI at the expense of the its foreign reserves as happened in 2014-16.

Moreover, these measures would only postpone and not resolve the crises, needing much higher oil prices to contain or mask it like in 2017-19. Medium-term oil prices would probably (for Brent prices) settle within a range of $50-60/bbl, which should partially relieve the stress on the budget, but not the need to address its imbalance.

Iraq’s 2019 budget, initially proposed by the prior government, submitted with minor changes by the current government and approved by the current parliament, perpetuated the same deficiencies and weaknessess of all Iraq’s budgets since 2003. Crucially, it deepened the structural imbalance between the budget’s current and investment expenditures, in which public sector wages consumed an ever-increasing share of government revenues.

Moreover, it undermined and reversed most of the small, but essential, fiscal reforms agreed with the IMF in the 2016 Stand-By Agreement (SBA) to address this structural imbalance; and which needed considerable follow-up reforms over the years to put the country on a sustainable path to growth and reduce the economy’s vulnerabilities to the volatile oil market. The extent of these vulnerabilities came to the fore during the collapse in oil prices in 2014, and coupled with the cost of the ISIS conflict, this led to a sharp contraction to the non-oil economy in 2014-17.

Undeterred by these memories, the budget’s planners, buoyed by the bounty of higher oil revenues, from late 2017 embarked on an expansionary budget that magnified these very vulnerabilities. This was achieved by simultaneously reversing the growth of non-oil revenues and by increasing current spending. Non-oil revenues decreased in both absolute terms and as a percentage of total revenues: -18% and -29% respectively in 2019 and 2018.

Additionally, 25% of these non-oil revenues were in fact oil-related in the form of taxes on foreign oil companies and the budget’s share from profits from the state’s oil companies. Current spending increased by 15% with the salary and pensions component growing by 7.5% instead of decreasing continuously.

The budget’s trumpeted increase of 29% in investment spending hides the fact that only 43% of this total spending for 2019 was earmarked for non-oil investment, which would nevertheless increase by 43% in 2019. However, historically this spending is on paper only, with an execution rate of under 65%. The performance in 2019 was much worse than normal with non-oil investment spending at about IQD 3.3 trn as of November 2019 from a planned budget of IQD 14.0 trn, or about a 24% execution rate.

The budget planners’ aims for 2020 were for a continuation of the expansionary budget of 2019, which dismayed the IMF enough for it to issue a critical country report (19/248) – the first since 2004. Adding to the dismay was the fact that the government’s plan for fiscal probity was based on expectations of continued high oil prices, as well as sticking to its historic under-execution of the budget. Essential budget reforms to address the structural imbalance were delegated to an expression of interest for inclusion in medium term fiscal strategy planning.

The IMF then modelled for a 2020 budget with revenues estimated at IQD 113.1 trn based on oil price assumptions of $55.8/bbl. Expenditures were estimated at IQD 123.2 trn, made up of current expenditures at IQD 99.1 trn, while oil investment spending was estimated at IQD 15.5 trn and non-oil investment spending at IQD 8.6 trn. This would have needed debt financing of IQD 10.0 trn to balance the budget. Since it’s almost impossible to cut the bulk of current spending, the government must have been anticipating a better budgetary situation through Iraqi oil prices higher than $55.8/bbl and from under-executing much needed non-oil investment spending and reconstruction.

By October, plans for budget expenditure ballooned by 31% to IQD 162.0 trn, necessitating debt financing of IQD 48.9 trn. While there are no details apart from spending and deficit figures, the political paralysis following the failure of the prime minister-designate to form a government in early March has put a halt to these runaway expenditure plans.

As long as the political class’ existential fear from the five-month long youth-led countrywide demonstrations continues to ebb and flow, this political paralysis is likely to continue. However, the main economic consequences would be the same whether a new government forms under a new prime minister-designate, or if the current caretaker government continues to limp on. The outcome either way will be that no new budget will be passed, with the government continuing to implement the executed parts of 2019’s budget throughout 2020 according to the ‘1/12th rule’.

Essentially, this means the government will continue to spend (per month) 1/12th of the actual spend in 2019 – effectively extending the current spending component for 2019 in addition to the increased spending of IQD 10.5 trn as a result of government measures to appease the demonstrators in October 2019. The government will likewise continue with the investment projects initiated in 2019.

Estimating the effects of the current events on the Iraqi budget is fraught with uncertainty. Current predictions on the extent of the decline in oil prices mirror those made following the 2014 oil price war, which then assumed a continuation of the decline into the future. This in time proved to be overly pessimistic, as will the current ‘worst-case’ prognoses. Moreover, though the effects of the new coronavirus on the world economy will be profound in Q1/2020, the extent and the continuation of these effects for the rest of the year remains uncertain.

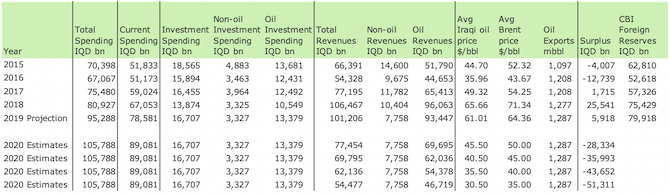

However, these negative effects would be compounded for oil prices by a sharply increased supply in an environment of weakened demand. The upshot would be an extended period of lower oil prices. The table below looks at the budget for 2015-19 and estimates for 2020 based on different realised oil prices for 2020 as whole (please see footnote 2 for notes and assumptions used).

Table 2: Iraq’s budget 2015-20. Source: Iraq Ministry of Finance[2]

Past policies of spending oil revenues on expanding the public payroll and welfare spending, in the process depleting the country’s wealth without building its infrastructure, has resulted in an economy dependent on imports of goods and services, a stunted private sector and a labour market skewed towards public employment. This development has been at the root cause of successive countrywide demonstrations. The need to urgently restructure the budget’s structural imbalances will require painful reforms and a long adjustment period, and thus would need a buy-in by the population at large.

This, given the extent of the current anti-political elite protest movement and the scale of the repression of this movement, is unlikely without significant political reform.

[1] The percentage figures are made up of salaries, pensions and transfers. Transfers are mostly composed of welfare spending and transfers to State-Owned Enterprises (SOEs) which in turn are primarily for salary payments and support to SOEs. Source: IMF Iraq country reports 2004-19.

[2] Revenues and expenditures for 2015-19 sourced from Ministry of Finance (MoF). These figures constitute revenues and expenditures actually received/made at the time and not booked. As such they differ, sometimes significantly, from those provided by the IMF. The crucial difference being that they resemble an actual cash flow statement and not an income statement. This can be seen from the difference between the Ministry of Oil’s (MoO) revenue data which show sales made and the MoF’s data which how funds received which can lag actual sales.

Iraqi oil sales and average Iraqi oil price are taken from MoO website, while average Brent prices can be found here. CBI foreign reserves are as of end of 2019 and are found here. 2019 budget numbers are as of November 2019 and projected to continue into end of 2019. Oil revenues are based on MoO data which are available as of the end of December 2019. The 2020 budget numbers assume a continuation of the budget spent for 2019. It is assumed that Iraq would maintain market share through aggressive pricing and thus that the discount to Brent would increase from $3.35 for 2019 to $4.50.

Disclaimer: Ahmed Tabaqchali’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any fund or security or to adopt any investment strategy. It does not constitute legal or tax or investment advice. The information provided in this material is compiled from sources that are believed to be reliable, but no guarantee is made of its correctness, is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding Iraq, the region, market or investment.

I – Legal and Institutional Framework Governing Extractive Industry Sector in Iraq;

II – Revenue distribution;

III – Revenue volatility;

IV – Government spending.

Moreover, for each of the topics above mentioned, the research work endeavors to:

(a) Explain the current (up to 2015) state of affairs; and,

(b) Answer the questions listed for each topic.

Throughout the research the emphasis was on three important components:

Instruments, Policies and Institutions;

The constitution, various related laws, legal frameworks and modalities (Instruments);

Adopted polices, strategies, actions and plans (Policies) and involved state federal, regional or provincial entities, ministries, councils, committees and bodies (institutions).

Russia’s state oil company Rosneft has reportedly paid $250 million to an external consultant to help secure deals in Iraqi Kurdistan.

Bloomberg reports that Rosneft Trading SA in 2017 “entered into an advisory agreement with an external consultant for advisory services relating to Rosneft Group’s proposed concession agreement and Production Sharing Contracts (“PSCs”) with the Kurdistan Regional Government of Iraq (“KRG”)”.

Iraq’s Ministry of Oil has announced preliminary oil exports for February of 98,347,884 barrels, giving an average for the month of 3.391 million barrels per day (bpd), up from the 3.306 million bpd exported in January.

These exports from the oilfields in central and southern Iraq amounted to 95,805,196 barrels, while exports from Kirkuk amounted to 1,765,032 barrels, and from Qayara 488,825 barrels. Exports to Jordan were 288,831 barrels.

Revenues for the month were $5.053 billion at an average price of $51.374 per barrel.

Genel Energy is reportedly considering whether to expand its operations in Kurdistan and elsewhere.

CFO Esa Ikaheimonen (pictured) is quoted as saying that the company has net cash of about $100 million, is open to merger and acquisition opportunities.

Deceptive shipping practices are reportedly being used in an attempt to conceal cargoes of sanctioned Iranian fuel oil being shipped via the Iraqi port of Khor al-Zubair.

Writing in Lloyds List, Michelle Wiese Bockmann gives details of a network of shell companies running ‘dark’ tankers to transport the sanctioned fuel.

Iraq’s Ministry of Oil has announced final oil exports for January of 102,485,591 barrels, giving an average for the month of 3.306 million barrels per day (bpd), down from the 3.428 million bpd exported in December.

These exports from the oilfields in central and southern Iraq amounted to 101,062,366 barrels, while exports from Kirkuk amounted to 1,114,035 barrels. Exports to Jordan were 309,190 barrels.

Revenues for the month were $6.163 billion at an average price of $60.139 per barrel.